Paying the Price of the Poverty Premium

It costs more to be poor

By Rev. Chris Frazer, Deacon for Social Justice with the Anglican Parish of Lower Hutt and the Wellington Cathedral of St Paul.

"There is enough in the world for everyone's need, but not enough for everyone's greed."

— Mahatma Gandhi

Introduction

The poverty premium (or poverty penalty) is the concept that people on low incomes pay more for the same essential goods and services than those who are financially better off. It represents a monetary disadvantage where the lack of upfront capital or lower creditworthiness forces individuals into more expensive payment methods or higher-cost products.

The concept of the poverty premium was first raised in 1963 by David Caplovitz, an American sociologist. In his book The Poor Pay More, he argues that people with low incomes pay more for essential goods and services such as food, clothing and credit.

The boots theory, coined by English fantasy writer Sir Terry Pratchett in his 1993 novel Men at Arms, has further highlighted the growing issue of socioeconomic unfairness. His novel features Captain Sam Vimes, who ponders on the cost of a pair of boots.

Gandhi's words are a powerful reminder that distribution, not a total lack of resources, drives poverty and environmental issues. The Earth provides enough resources for everyone's basic needs (food, shelter, water), but infinite greed leads to inequality and scarcity, highlighting sustainability and ethical consumption over endless accumulation.

The reason that the rich were so rich, Vimes reasoned, was that they managed to spend less money. Take boots, for example. He earned thirty-eight dollars a month plus allowances. A really good pair of leather boots cost fifty dollars. But an affordable pair of boots, which were sort of OK for a season or two and then leaked like hell when the cardboard gave out, cost about ten dollars. Those were the kind of boots Vimes always bought, and wore until the soles were so thin that he could tell where he was in Ankh-Morpork on a foggy night by the feel of the cobbles.

But the thing was that good boots lasted for years and years. A man who could afford fifty dollars had a pair of boots that'd still be keeping his feet dry in ten years' time, while the poor man who could only afford cheap boots would have spent a hundred dollars on boots in the same time and would still have wet feet.

In New Zealand, the poverty premium is not a single, quantifiable amount but a set of costs and disadvantages faced by low-income households. This premium arises from systemic issues like limited access to savings, higher costs for essential goods, and reliance on expensive credit options to manage daily and unexpected expenses.

Key factors that contribute to the poverty premium

Higher cost of borrowing

People and families with low incomes often cannot access mainstream, low-interest credit options and are forced to use high-cost alternatives like payday loans or certain Buy Now, Pay Later schemes to buy gifts and food. While the Credit Contracts and Consumer Finance Act limits total repayments to no more than twice the amount borrowed for high-cost loans, the interest and fees still add significant expense compared to interest-free or low-interest options available to wealthier individuals.

Financial inability to take advantage of time-limited special offers

People with higher incomes are able to buy items in bulk, shop during sales like Black Friday, and benefit from early-bird specials, which require upfront cash. Low-income households often cannot afford to take advantage of these savings and may end up paying full price for items closer to certain times of the year, such as Christmas, when demand and prices can be higher.

Insurance costs

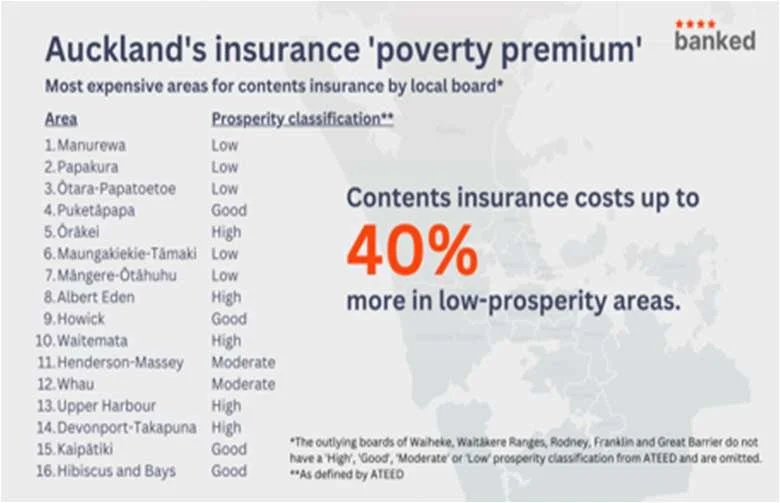

Contents insurance can cost up to 40% more in low-prosperity areas of Auckland

Research in New Zealand has shown that contents insurance can cost up to 40% more for Kiwis in low-prosperity areas of Auckland, even though they are less able to benefit from multi-policy or prompt-payment discounts. This means poorer families pay more for the same protection, a factor that adds to general financial strain and limits their ability to build a financial buffer for seasonal pressures.

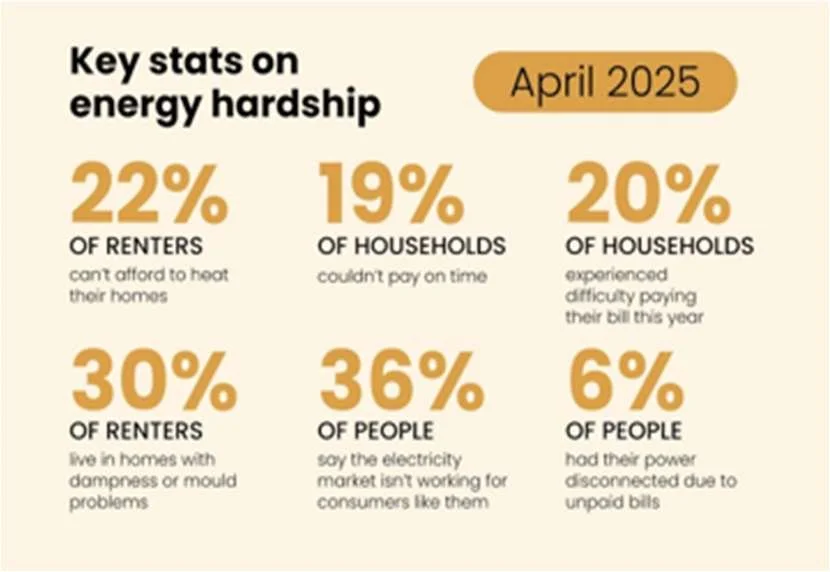

Key statistics on power poverty in New Zealand

Paying the price of power

Research undertaken by Consumer NZ in 2025 revealed that more New Zealanders have found themselves unable to pay their power bills on time, signalling a growing strain on household budgets. Missed payment deadlines are becoming more common, and for many, the consequences extend beyond temporary inconvenience.

Fifteen percent of consumers reported paying overdue fees in the past year — a clear example of the poverty premium, where those already under financial pressure end up paying more simply because they cannot meet payment deadlines. As financial stress deepens, many households are turning to their personal networks for support.

Fourteen percent of New Zealanders said they relied on family or friends to help cover their power bill, highlighting the increasing role of informal safety nets in meeting essential costs. But not everyone has someone to turn to. Seven percent of respondents had to take out a loan to keep up with their electricity payments, exposing them to interest charges and further financial risk.

Meanwhile, one in ten sought government assistance to avoid disconnection, underscoring how essential energy hardship has become a reality for a significant share of the population.

These pressures are shaping public reaction. Just over one-third of New Zealanders believe the electricity market is working poorly for consumers like them. Given the rising number of missed payments, the reliance on borrowing, and the growing need for government support, this perception reflects more than dissatisfaction — it points to a system that many feel is no longer meeting their needs.

Together, these findings paint a picture of increasing vulnerability. As more households struggle to stay connected, the compounding costs of financial hardship are becoming harder to ignore. The data suggests that without meaningful change, the gap between what consumers can afford and what the electricity market demands will continue to widen.

The overall financial strain during such times as the holiday period can lead to high levels of stress, which can affect long-term decision-making and push families further into a cycle of debt. Budget advisors often see increased demand for services after Christmas and at the beginning of the school year when families face "back-to-school" expenses on top of holiday debt.

Overall, the poverty premium means that it simply costs more to be poor, and these extra costs are magnified during peak spending times like Christmas, making it difficult to avoid a financial fallout.

The poverty premium — the higher costs low-income households pay for essential services, goods, and credit — functions as more than just a financial penalty; it causes severe, intangible damage through reduced agency and deep humiliation. This hidden cost creates a cycle of shame and hopelessness that acts as an emotional tax on wellbeing.

The hidden costs and harsh reality of the poverty premium

The reality of daily living within the 'premium' struggle

The poverty premium functions as more than just a financial penalty; it causes severe, intangible damage through reduced agency and deep humiliation. This hidden cost creates a cycle of shame and hopelessness that acts as an emotional tax on wellbeing.

The experience of poverty is described as a "cumulative tax paid daily" that ruins peace of mind and dignity, extending far beyond a simple lack of money.

The constant "economic trade-offs" often come at the expense of mental health, causing chronic stress, anxiety, and depression. These intangible impacts can cause people to avoid accessing essential services — like healthcare or financial products — due to fear of stigma, thereby perpetuating the poverty cycle. There is a danger that such constant financial worry reduces life to the immediate: "How do I pay my overdue bill?" "How can I secure enough food to feed my children?" "How can I be there to support my wider whānau, when they call out for help?"

Such day-to-day struggles limit a person's or family's capacity to engage in long-term planning.

Humiliation and the loss of agency

Feeling shame in daily transactions: The need to rely on charity, such as food banks, creates a profound sense of shame and embarrassment.

Social isolation: Financial stress can lead to detaching oneself from community engagement due to the stigma of not being able to afford social norms.

Self-blame and helplessness: The constant struggle can lead to a loss of self-worth, with individuals feeling "worthless" or blaming themselves for systemic disadvantages, which are often structural, not personal failures.

Treatment in institutions: People living on a low income may encounter degrading and judgmental treatment in public service settings, adding humiliation to the material hardship of poverty.

Poverty is not a moral failure; indifference is.

Reflection

The parable of the Good Samaritan, found in the Gospel of Luke chapter 10:25–37, shows us clearly that true Christ-centred compassion crosses boundaries. In this parable, God's provision for the injured man comes through the kindness and practical care of a foreign traveller. As we read through the parable, we hear how:

- He saw the man.

- He stopped.

- He acted.

- He paid the cost.

- He followed through.

Compassion is not a feeling — it is a costly, boundary-breaking commitment.

God stands with those who are poor and disadvantaged. Jesus identifies with those on the margins of society. The Spirit empowers the church to stand alongside and to serve those in need. Therefore, to follow Christ is to stand where He stands.

What steps might we begin to take to actively address the cost of the poverty premium on a growing number of our whānau within Aotearoa today? Maybe a good start will be to undertake:

- One concrete act of generosity this week.

- Discuss one structural change we may pursue as a church.

- Explore relationships we can deepen with organisations working to alleviate hunger and poverty among those left on the margins of our society today.

Whilst our government, alongside businesses and organisations, have a key role to play right now in addressing the effects of the poverty premium on vulnerable people and families, so do we!

So, will you come on board? Together we can make a real difference!

"The compassion we seek is to stand in awe at what the poor have to carry, rather than in judgment at how they carry it."

— Fr. Greg Boyle

References

1. Mahatma Gandhi.

2. Men at Arms, novel, 1993. Author Sir Terry Pratchett.

3. Consumer NZ — [Power poverty persists](https://www.consumer.org.nz/home-and-living/home-energy/power-poverty-persists#escalating-concerns-about-energy-costs).

4. Voices of the Poor, World Bank research, March 2000.

5. Fr. Greg Boyle, "The compassion we seek is to stand in awe at what the poor have to carry, rather than in judgement at how they carry it."